Scale exposes cracks. “Fintech A” (a pseudonym for a leading U.S. consumer lending platform) reached a tipping point. They had scaled to 1 million users, but their support operation was collapsing. They were relying on a patchwork of in-house agents in San Francisco (too expensive) and a low-cost offshore BPO in Manila (too disconnected).

The Breakdown:

- CSAT Dropped: From 4.8 to 3.2 in six months.

- Compliance Risk: Agents were skipping IDV (Identity Verification) steps to keep up with volume.

- Attrition: In-house agents were burning out; offshore agents were churning every 90 days.

The Pivot: Nearshore First-Party Model

The COO made a strategic decision to move to a specialized Nearshore model in the Dominican Republic, but with a specific mandate: Do it as a First-Party extension.

The Implementation:

- Recruiting for Profile: They hired agents with 2+ years of collections experience, not just generic support.

- Integrated Systems: They gave nearshore agents full access to the CRM (via secure VDI), enabling them to see the full customer journey.

- Shared Incentives: The vendor was bonused on Recovery Rate and QA Score, not just hours worked.

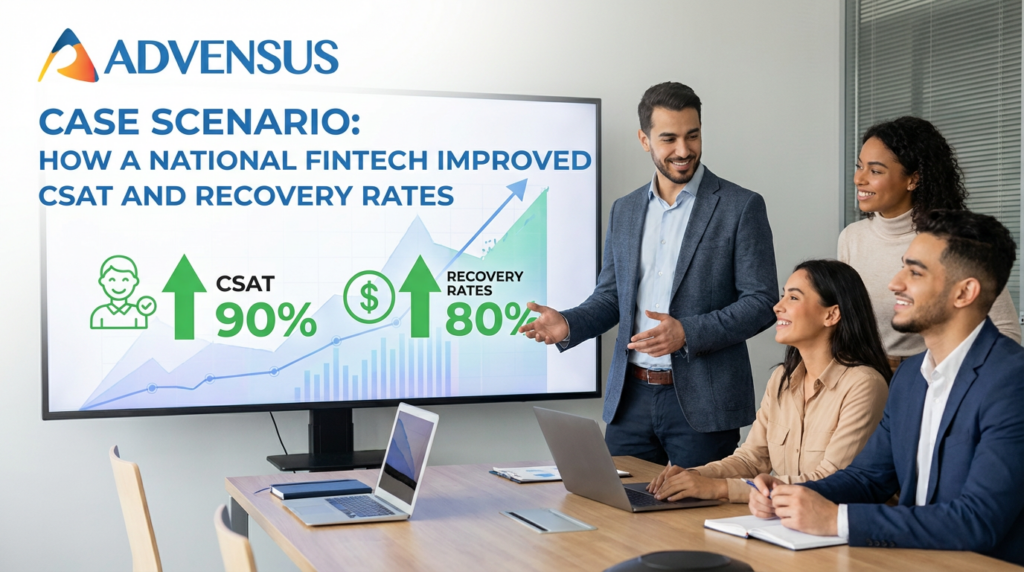

The Results (After 120 Days)

- CSAT Rebound: Stabilized at 4.6 within 4 months.

- Recovery Rate: Increased by 22% because agents could negotiate payment plans effectively in English.

- Cost Efficiency: They reduced their blended cost per hour by 40% compared to their previous hybrid model of US/Offshore.

Prepare your operation before scale forces reactive decisions. You don’t have to wait for the crash to fix the engine.

Conclusion

Fintech A proved that you can outsource without selling out. By choosing the right geography and the right engagement model, they turned a failing cost center into a stable growth engine.